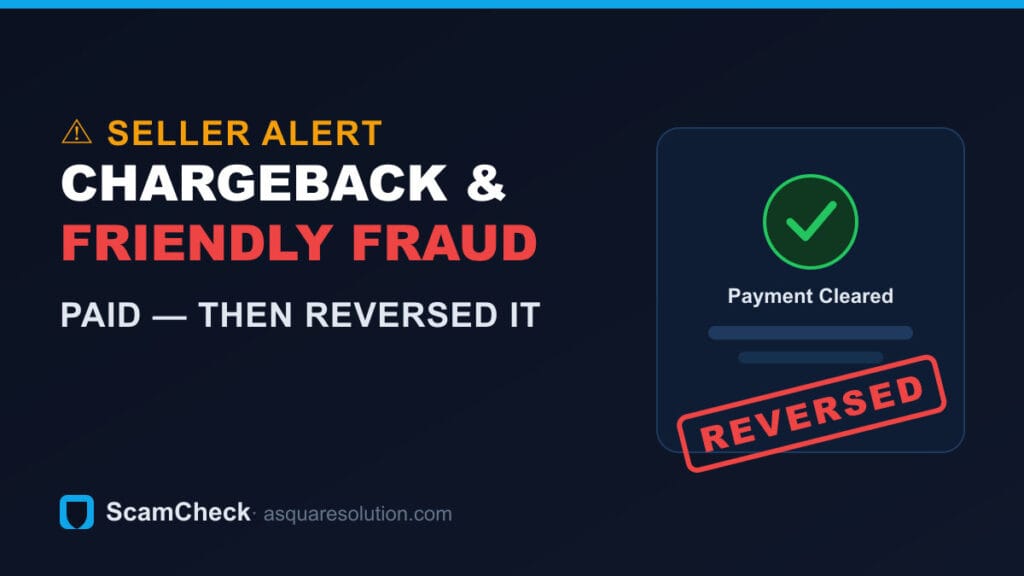

Not every payment scam uses a fake screenshot. In a chargeback scam — also called friendly fraud — the buyer really pays, receives the item, and then disputes or reverses the payment to get their money back while keeping the goods. This guide explains how it works, how it differs from a fake-payment scam, and exactly what a seller needs to fight it.

This is the other half of payment fraud. If your problem is a payment that never arrived, start with our guide on how to spot a fake payment screenshot instead — this page is about payments that did arrive and were later reversed.

Key takeaways

- In a chargeback / friendly-fraud scam the money really lands, then the buyer reverses it after getting the item — so there’s no fake screenshot to catch.

- Your defence isn’t detection, it’s documentation: tracked, signed delivery and a clear record of the sale.

- Chargebacks are most common on PayPal and card payments; instant P2P transfers (Zelle) are largely irreversible, which is why scammers prefer reversible rails.

Fake payment vs a real reversal — the crucial difference

These are two different problems, and confusing them costs sellers money:

- Fake payment scam. No money ever arrives. The “proof” is an edited screenshot or spoofed email. You beat it by verifying the payment in your own account before you ship.

- Chargeback / friendly fraud. The money does arrive — you see it, it clears, you ship. Days or weeks later the buyer files a dispute or card chargeback (“item not received,” “not as described,” or “I didn’t authorize this”) and the payment is pulled back. You beat this one with evidence, not verification.

So confirming the payment landed — the rule that stops fake screenshots — does not protect you from a chargeback. A real, cleared payment can still be reversed.

How the chargeback scam works, step by step

- A genuine payment. The buyer pays with a card, PayPal, or a card-funded transfer — the money really reaches you.

- You ship in good faith. Everything looks clean, so you send the item.

- The dispute. After delivery, the buyer contacts their bank, card issuer, or PayPal and claims the charge was unauthorized, the item never arrived, or it was “not as described.”

- The reversal. The payment is provisionally pulled back (often plus a dispute fee), and you must prove your case to get it back.

- The outcome. Without solid proof of delivery and the transaction, the reversal usually stands — the buyer keeps the item and the money.

Where chargebacks show up

- Credit / debit cards. The classic chargeback — the cardholder disputes the charge with their issuer. Even a completed sale can be reversed long after delivery (card chargeback windows are often around 120 days, but vary by network and reason — check the current rules).

- PayPal. Buyers can open a PayPal dispute or a card chargeback through PayPal. As our PayPal guide notes, even a “Completed” Goods & Services payment can be reversed — and Friends & Family payments give you no seller protection at all.

- Marketplace platforms. eBay, Etsy and similar buyer-protection programs let buyers open “item not received” or “not as described” cases that function like chargebacks.

- Cash App / Venmo / Zelle. Standard person-to-person payments are largely irreversible — but if the buyer funded it with a card, the card issuer can still chargeback. This is a big reason scammers steer you to “just send it as a normal payment.”

The friendly-fraud playbook: the three claims

- “Item not received.” Beaten by tracked delivery with proof of receipt.

- “Not as described.” Beaten by clear photos, the listing text, and your messages.

- “I didn’t authorize this.” The hardest — beaten by proof it was the cardholder (matching name/address, signature, comms).

What proof a seller should keep

Chargebacks are won or lost on documentation. Before and during every sale, keep:

- Tracked shipping with delivery confirmation — and signature on delivery for anything valuable.

- Proof the address matches the payer — ship only to the confirmed address on the payment.

- Photos of the item and packaging before it ships (condition, serial numbers, contents).

- The full conversation — the agreement, the listing, and any messages, saved as screenshots.

- The transaction record — date, amount, payment method, and reference/transaction ID.

What to do if a buyer disputes after receiving the item

- Don’t ignore it. Respond to the dispute within the deadline — missing it is an automatic loss.

- Submit your evidence. Upload tracking with proof of delivery/signature, photos, the listing, and messages. This is called representment on cards.

- Cite protection where it applies. If you used PayPal Goods & Services and shipped to the confirmed address with tracking, you may be covered by PayPal Seller Protection. Check eligibility and reference it.

- Escalate / appeal. Use the platform’s appeal process; for card chargebacks the issuer decides based on the evidence both sides submit.

- Report repeat offenders to the marketplace and, for clear fraud, to the authorities (see below).

How to reduce chargeback risk before it happens

- Take protected payments (PayPal Goods & Services, card via a proper processor) — never Friends & Family for a sale.

- Always ship with tracking, and require signature for high-value items.

- Ship only to the confirmed payment address — never a “send it here instead” request.

- For local, high-value deals, prefer cash in person, which can’t be charged back.

- Watch for overpayment and rushed-buyer behaviour — friendly fraud often travels with other Marketplace scam patterns.

Where ScamCheck fits — and where it doesn’t

Be clear about this: ScamCheck can’t reverse a chargeback. A chargeback on a real payment is a documentation-and-dispute problem, not a screenshot problem — no tool detects a “fake” payment here, because the payment was genuine. Where ScamCheck does help is the other, more common half of seller fraud: when a buyer sends a fake “payment sent” screenshot and no money ever arrives. Before you ship, if the “proof” is an image rather than money in your account, that’s exactly what ScamCheck is for.

Not sure a “payment” screenshot is even real?

That’s the half you can catch up front. Upload the image to ScamCheck’s free AI screenshot detector — it flags an edited or fake “payment sent” screen in seconds, before you ship. (It won’t help with a chargeback on a real payment — for that, keep the proof above.)

Selling to an unfamiliar buyer or business? Verifying the payment is only half the check — and for higher-value orders, knowing who you’re dealing with reduces dispute risk. See whether a business is independently verified with TrustSeal.

If you’ve been hit by a chargeback scam

- Respond to the dispute with your evidence before the deadline — don’t let it lapse.

- Report the buyer to the marketplace or platform; flag repeat “item not received” abuse.

- For clear fraud, file with the FTC (US) or Action Fraud (UK), and the FBI IC3.

- Keep every record — issuers and platforms decide on documentation.

Get a 2-minute seller scam heads-up

New payment scams spread fast. Get short email alerts on fake screenshots, chargebacks, and overpayment traps — unsubscribe anytime.

Frequently asked questions

Can a buyer reverse a payment after I’ve shipped the item?

Yes. Card payments and PayPal Goods & Services payments can be disputed and reversed well after delivery (card chargeback windows are commonly around 120 days, though this varies). A cleared payment is not a final payment — which is why proof of delivery matters.

What is friendly fraud?

Friendly fraud is when a real customer disputes a legitimate charge to get their money back while keeping the goods — falsely claiming the item never arrived, wasn’t as described, or wasn’t authorized.

Can I win a chargeback as a seller?

Often yes, if you submit strong evidence on time: tracking with proof of delivery (signature for valuable items), the listing, photos, and your messages. “Item not received” claims are the most winnable when you have signed delivery.

Does PayPal always side with the buyer?

Not always. PayPal Seller Protection may cover eligible Goods & Services sales shipped with tracking to the confirmed address — check PayPal’s current Seller Protection terms, as coverage and conditions change. Friends & Family payments have no protection, so never use them for a sale.

Are Zelle, Venmo and Cash App chargeback-proof?

Standard person-to-person payments are largely irreversible, but a card-funded transfer can still be charged back by the card issuer. Treat “send it as a normal payment” requests with caution.

Handling chargebacks and payment disputes at scale?

If fake payments, chargebacks and dispute admin have become a real cost for your business, they can be automated. A Square Solutions builds custom fraud-prevention and chargeback-defense systems — from the team behind ScamCheck and TrustSeal.

Related payment-scam guides

- How to spot any fake payment screenshot (complete guide)

- How to verify a payment before you ship

- Facebook Marketplace payment scams

- Overpayment / “refund the difference” scam

- Fake PayPal payment screenshot

- ScamCheck: free payment-screenshot detector