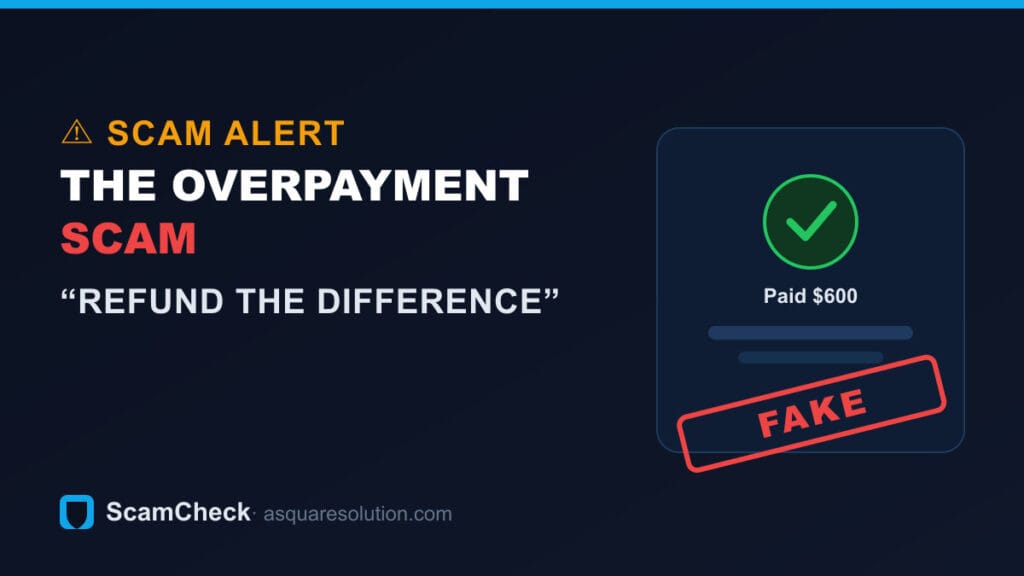

The overpayment scam is simple and brutal: someone “accidentally” pays you too much with a fake or reversible payment, then asks you to send back the difference. You refund real money — and their original payment never actually clears. Here’s how it works step by step, and how to make sure you never lose a cent to it.

New to this? Start with our complete guide on how to verify any payment screenshot — the rule below applies to every app and country.

Key takeaways

- The refund you send is real; the “overpayment” you received is fake or reversible.

- It shows up in marketplace sales, rental deposits, fake job/“equipment” offers, and check payments.

- Never refund from a payment until it has fully cleared in your own bank or app — not just “pending” or shown in a screenshot.

How the overpayment scam works, step by step

- Contact. A “buyer,” “tenant,” or “employer” agrees to a deal and moves quickly to payment.

- The overpayment. They send you more than agreed — via a doctored screenshot, a fake “pending” email, a check, or a card-funded transfer.

- The “mistake.” They message in a panic: they “overpaid by accident,” or the extra was “meant for the mover / supplier.”

- The pressure. They urgently ask you to refund the difference — often to a different account than the one that paid.

- The reversal. You send a real refund. Days later the original payment bounces, is cancelled, or is clawed back — and your refund is gone. That clawback works like a chargeback / friendly-fraud reversal.

What “refund the difference” pressure looks like

The messages are designed to make you act before you think:

- “So sorry — I typed $600 instead of $60. Can you send the $540 back? I’m really stressed about it.”

- “The extra is for the courier — please forward it to them so pickup isn’t delayed.”

- “My assistant paid twice by mistake, can you refund one? I’ll leave great feedback.”

Notice the pattern: urgency, an emotional or plausible reason, and a request to move real money out before the incoming payment could possibly have cleared.

Common versions

- Marketplace overpayment. “I sent $500 instead of $300 — can you send $200 back?” on an item that was never really paid for.

- Fake check overpayment. A check for more than the price; the bank “makes funds available” before it clears, then reverses it days later.

- Rental / deposit overpayment. A “tenant” overpays a deposit and asks for the difference back before moving in.

- Job / task overpayment. A fake employer sends money for “equipment” and asks you to forward part to a “vendor.”

How fake payment proof fits in

The overpayment scam almost always rides on fake proof. The scammer shows a screenshot of the “$600 sent,” or forwards a spoofed “payment received — funds pending” email designed to look like it’s from PayPal, Zelle or your bank. Your own account tells a different story: either nothing arrived, or it’s pending and reversible. That gap between the screenshot and your actual balance is the whole scam. Learn how to read a payment screenshot and you defuse it instantly.

Red flags

- Any payment that arrives higher than agreed, followed by a request to send money back.

- Urgency and an emotional reason for the “mistake.”

- Refund requested to a different account, person, or method than the one that paid.

- Proof of the overpayment is a screenshot, email or check — not cleared funds in your account.

What to do if the money looks pending, reversible or suspicious

If an incoming payment is larger than agreed, or shows as pending / on hold, treat it as unpaid:

- Don’t send anything back. Not the difference, not a “fee,” nothing — until the original has fully and irreversibly cleared.

- Refund only via reversal. If there really was an overpayment, ask the sender to cancel or reverse their own payment; never send a separate transfer.

- Check with your bank before trusting “available” funds from a check or card — ask specifically whether it has settled, not just posted.

- When in doubt, cancel the whole deal. A genuine person will understand; a scammer will pile on pressure.

Got a payment screenshot you’re not sure about?

Upload it to ScamCheck’s free AI screenshot detector — it reads the image and flags the signs of an edited or fake “payment” screen in seconds. Use it as a second opinion, then still confirm the money in your own account.

Buying from an unfamiliar seller or business? Verifying the payment is only half the check — verify the seller too. See whether a business is independently verified with TrustSeal.

If you’ve already been scammed

- Report it to the marketplace or platform where it happened and to your payment app right away — and ask whether the payment can be frozen or reversed.

- File with the FTC at reportfraud.ftc.gov (US) or Action Fraud (UK).

- Report to the FBI IC3 at ic3.gov.

- Save every message, the screenshot, the buyer’s profile and the account details as evidence.

Get a 2-minute seller scam heads-up

New payment scams spread fast. Get short email alerts on fake screenshots, chargebacks, and overpayment traps — unsubscribe anytime.

Frequently asked questions

Why is the overpayment scam so effective?

Because your refund uses real, cleared money, while the “overpayment” is fake or reversible. Banks often show incoming funds as available before a check or card payment truly settles, creating a false sense that the money is yours.

What should I do if a buyer overpays me?

Don’t send anything back. Ask them to cancel or reverse the original payment, or cancel the sale entirely. Only refund after the funds have fully and irreversibly cleared in your account.

Is a screenshot of an overpayment proof that I was paid?

No. A screenshot proves nothing — verify the exact amount in your own account before you act.

How long before a payment is truly safe to refund from?

Only once it has fully cleared — which for checks and some card-funded transfers can take days or even weeks. “Funds available” is not the same as “funds cleared.” When unsure, ask your bank directly.

Related payment-scam guides

- How to spot any fake payment screenshot (complete guide)

- Fake PayPal payment screenshot

- Fake Venmo payment screenshot

- Fake Cash App payment screenshot

- Fake Zelle payment / transfer screenshot

- ScamCheck: free payment-screenshot detector